BBO vs sales tax

Due to the recent increase of the BAZV tax and the introduction of the BAVP tax there is renewed confusion and discussion as to what the BBO really is and how to deal with it. In this short article we’ll try to explain this by comparing it to the US sales tax, which most Aruban business tend to compare it with.

The US sales tax

The US sales taxes are generally administered at the state level. In most states, sales tax is imposed on retail buyers and retail sellers are the collection agents who collect that money from buyers and remit it to the state. This is the sales tax that most of us know from the experience we have with the US. However, there are states (Arizona for example) that impose a sales tax on the retail seller. For the purpose of this article we will not be going into the details of this type of sales tax.

Sales tax is calculated by multiplying the purchase price by the applicable tax rate. Tax rates vary widely by jurisdiction and range from less than 1% to over 10%. Sales tax is collected by the seller at the time of sale. A sales tax is imposed only at the retail level. In cases where items are sold at retail more than once, such as used cars, the sales tax can be charged on the same item indefinitely.

Although the tax is technically due from the customer purchasing the item, the seller has the obligation to charge, collect, and remit the tax as an agent of the state.

BBO tax

Unlike the US sales tax explained above, the BBO tax was introduced as a sales tax on businesses (sellers) in that the BBO legislation does not obligate the business to charge, collect and remit the tax as an agent of the island. Naturally, businesses (sellers) would like to pass the cost of this tax on to their customers (buyers). Unfortunately, the BBO legislation did not define how businesses (sellers) would be allowed to pass this tax on to the customer (purchaser) and left this to the creativity of businesses to chose the method they thought was best.

Businesses (sellers) have the following choices:

- Businesses could decide not to pass this additional cost to their customers

- Businesses could increase their selling prices to include the additional cost

- Businesses could charge the BBO to their customers as a separate line on their invoices

1: Not passing the additional cost to their customers

This solution is probably the least used (if at all) because the purpose of every business is to make a profit. If a new tax is imposed onto the business which will affect its profit, it is only natural that they would want to find a way to cover this additional structural cost somehow.

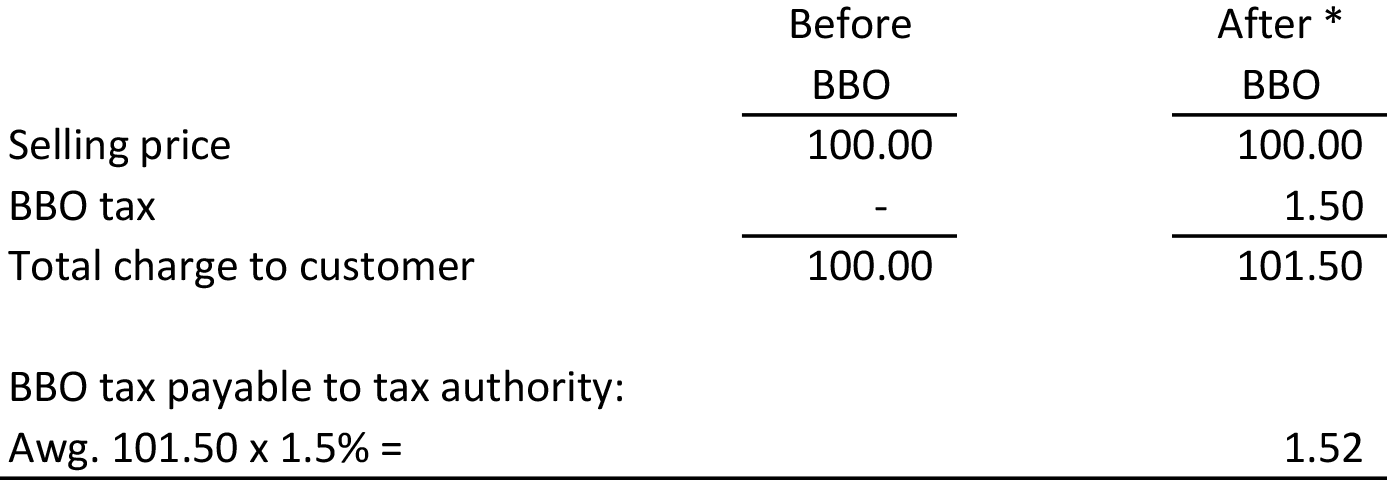

2: Increase the selling price

Businesses could increase their selling price with a certain percentage to account for the increase in their cost (the BBO tax that they as the business (seller) will now have to pay to the tax authorities). The situation will look as follows:

3: Charge the BBO as a separate line

This is probably the most used method to pass the cost of the BBO tax on to your costumers because most POS systems and accounting software already have the feature built-in. This is also a way for businesses to be transparent about the way they pass on the cost of the BBO to their customers.

In passing down the cost of the BBO to the customers came also the first striking difference between the US sales tax and the BBO. The tax authority was quick to point out that businesses were allowed to charge their customers the BBO tax but that this charge would also constitute part of their business turnover (sales). Consequently, businesses would have to pay BBO tax on the BBO tax that they had charged to their customers.

This argument was cemented in a court of appeals decision for tax cases. In this court decision it was pointed out that the explanatory memorandum (Memorie van Toelichting) of the BBO legislation stated that the government had chosen for a BBO tax system similar to that of other Dutch islands (Sint Maarten, Sint Eustatius and Saba). In these other Dutch islands, the BBO tax due to the tax authority is calculated on the total amount businesses received for the goods they sold or services they provided to customers. This total amount included any BBO charge the business charged their customers.

In the original BBO legislation proposal it was even stated that it was forbidden to state the BBO on the invoice to the customers. This would have eliminated the option to charge customers the BBO on a separate line on the invoice (option 3). This part of the legislation was questioned and criticized by both the Aruban Association of Tax Consultants (AATC) and the Aruban Advisory Board (Raad van Advies: RVA). The AATC cited that it was in the benefit of transparency to allow the BBO to be stated on the invoice to prevent additional price increase above the BBO percentage. The RVA even suggested to make it mandatory to state the BBO on the invoice for transparency reasons and in order to gain some insight in how businesses were passing the cost of the BBO within the supply chain.

Another big difference between the two sales tax systems is that unlike the US sales tax which is only imposed at the retail level, the BBO is imposed at every level of the supply chain. The wholesaler will have to pay BBO tax on its sales to the supermarket. The supermarket will have to pay BBO tax on its sales to the restaurant. The restaurant will have to pay BBO tax on its sales to its customers. This had a cumulative effect in that items were taxed at (sometimes up to) 3 different levels. This was the feature that was most criticized about the BBO tax.

The BBO tax rate had originally started at 3% at the beginning of 2007 but was later reduced to 1.5% in 2010. In the years after that the government introduced an additional tax called the BAZV tax that was to assist in covering the costs of the government medical insurance plan. This started at 1% and was later increased to 2%. In July 2018 the government introduced another tax called the BAVP tax at a rate of 1.5% and increased the BAZV tax to 3%. As of this writing the BBO/BAZV/BAVP taxes are as follows:

[table id=1 /]

The legislation of the BBO, BAZV and BAVP tax are basically the same. However, there is an interesting difference in the BAZV tax legislation. Unlike the BBO and BAVP legislation, article 15 of the BAZV legislation explicitly states that the business must state the BAZV amount payable by the business to the tax authority on the invoice/receipt. This article also created a lot of confusion in the Aruban business community. Many businesses rightly assumed that the tax legislation directed them to state the BAZV tax that was being charged to the customer on the invoice/receipt. As mentioned earlier many POS systems and accounting software already had a feature that could easily do this. However, the tax legislation actually directs businesses to state the BAZV tax that the business will have to pay to the tax authority on that particular sale. This is not only an odd requirement but also harder to comply with since most POS systems and accounting software do not have this feature built-in and do not allow this kind of customization.

One final question we like to discuss here was whether it is allowed to charge another rate other than the 6% (total). The answer is yes. As we mentioned above, the BBO legislation did not define how businesses would be allowed to pass this tax on to the customers (purchasers) but left this to the creativity of the businesses. This created some confusion and frustration among customers. For example, it is now harder to see right away which supermarket has the cheapest price on a particular item because one supermarket might have included the BBO/BAZV/BAVP in its prices while the other adds the BBO/BAZV/BAVP at the bottom of the invoice as a separate line.